Here is an interesting story that I came across the other day:

http://www.braylonedwards.com/media/braylon-edwards-former-cleveland-browns-wide-receiver-gives-10000-scholarships-to-100-cleveland-schools-students/

How cool is that? Of the 100 kids in this program, 79 went off to college this year which means that Edwards paid $790,000 in scholarships, not to mention the laptops and clothes he gave out with the scholarships. Maybe you are thinking, "He is an athlete. He probably makes millions of dollars a year." Well Edwards made $1,000,000 this year which means he gave away more than 75% of his salary. Pretty impressive. I always thought Edwards was just another thug in the NFL, especially after this, but I'll tell you what, this is definitely not a case of Scott's Tots. Edwards came up big and I wish more athletes would do this.

Friday, December 23, 2011

Monday, November 21, 2011

What Funds To Buy For Your Couch Potato Portfolio

One of the best places to buy funds at is Vanguard because of the extremely low fees (on average about .21%, which is $2.10 per $1,000) and high quality funds. Plus, if you open a Vanguard account, there are no fees when you trade, so you can save quite a bit of money over time.

Here is what I suggested in my last post for your Couch Potato Portfolio:

Name Percent of Portfolio

S&P 500 13%

U.S. Value 20%

U.S. Small Cap 12%

U.S. Small Cap Value 10%

U.S. Midcap 10%

Total International 25%

Emerging Markets 5%

REIT 5%

Now here are the exact funds from Vanguard that I recommend:

S&P 500 - Vanguard S&P 500 ETF (VOO)

U.S. Value - Vanguard Value ETF (VTV)

U.S. Small Cap - Vanguard Small-Cap ETF (VB)

U.S. Small Cap Value - Vanguard Small-Cap Value ETF (VBR)

U.S. Midcap - Vanguard Mid-Cap ETF (VO)

Total International - Vanguard Total International Stock ETF (VXUS)

Emerging Markets - Vanguard MSCI Emerging Markets ETF (VWO)

REIT - Vanguard REIT ETF (VNQ)

*ETF's have no minimum money requirement to invest, as opposed to most mutual funds which make you invest at least a few thousand dollars to start in each fund (which is money most of us don't have).

The most important thing is that after you buy this portfolio, you need to leave it alone! When I say leave it alone, I mean don't buy and sell funds just because something bad happened in the news because you are thinking on such a short-term basis. Remember, this portfolio is for the long hall (30+ years), and what happens on a single day or two is not going to matter in the grand scheme of things. It is impossible to consistently time (and beat) the market, so don't even try (or you will lose lots of money!). The only thing that you can and should do is add money to these funds through a method called Dollar-Cost Averaging (DCA). For this technique, you buy a fixed dollar amount of a particular investment on a regular schedule, regardless of the share price. More shares are purchased when prices are low, and fewer shares are purchased when prices are high. This is a good technique because it takes some of the emotion out of investing.

So again, buy this portfolio, or one very similar to it, and leave it alone until you retire. You will thank me when everyone else is stressing about retirement.

Here is what I suggested in my last post for your Couch Potato Portfolio:

Name Percent of Portfolio

S&P 500 13%

U.S. Value 20%

U.S. Small Cap 12%

U.S. Small Cap Value 10%

U.S. Midcap 10%

Total International 25%

Emerging Markets 5%

REIT 5%

Now here are the exact funds from Vanguard that I recommend:

S&P 500 - Vanguard S&P 500 ETF (VOO)

U.S. Value - Vanguard Value ETF (VTV)

U.S. Small Cap - Vanguard Small-Cap ETF (VB)

U.S. Small Cap Value - Vanguard Small-Cap Value ETF (VBR)

U.S. Midcap - Vanguard Mid-Cap ETF (VO)

Total International - Vanguard Total International Stock ETF (VXUS)

Emerging Markets - Vanguard MSCI Emerging Markets ETF (VWO)

REIT - Vanguard REIT ETF (VNQ)

*ETF's have no minimum money requirement to invest, as opposed to most mutual funds which make you invest at least a few thousand dollars to start in each fund (which is money most of us don't have).

The most important thing is that after you buy this portfolio, you need to leave it alone! When I say leave it alone, I mean don't buy and sell funds just because something bad happened in the news because you are thinking on such a short-term basis. Remember, this portfolio is for the long hall (30+ years), and what happens on a single day or two is not going to matter in the grand scheme of things. It is impossible to consistently time (and beat) the market, so don't even try (or you will lose lots of money!). The only thing that you can and should do is add money to these funds through a method called Dollar-Cost Averaging (DCA). For this technique, you buy a fixed dollar amount of a particular investment on a regular schedule, regardless of the share price. More shares are purchased when prices are low, and fewer shares are purchased when prices are high. This is a good technique because it takes some of the emotion out of investing.

So again, buy this portfolio, or one very similar to it, and leave it alone until you retire. You will thank me when everyone else is stressing about retirement.

Saturday, November 19, 2011

The Couch Potato Portfolio

After poring over hundreds of articles, reading dozens of books, and listening to hours upon hours of lectures about investing, one thing becomes clear: it is very, very hard to beat the market over a long period of time. Do you really expect to beat the market repeatedly by buying that "hot" stock? Come on now. Turns out, stocks that are out of favor with people have a better return than the "hot" stock over the course of history. So where does that leave you? How are you supposed to invest intelligently when you aren't poring over financial statements all day long? The answer is called the Couch Potato Portfolio.

The key to this portfolio is diversification and the way you do that is by buying low-cost mutual funds/Exchange Traded Funds (ETFs) (these are made up of many stocks instead of individual stocks) across many different asset classes and from all over the world. You can't just buy the huge companies that we have all heard of, like Apple and Wal-Mart, because there isn't enough growth left in those businesses. Did you know that historically, those small companies that no one has every heard of have produced a better return than those big companies? Well it's true. Check out this chart that shows how much $1 invested across a given asset class in 1926 would have grown in the next 80 years. Small stocks clearly provide a greater return than large stocks historically. And you can't focus solely on American stocks because the United States' economy is already established and is growing at a much slower pace than over 100 countries around the world so it is wise to invest internationally (lucky for us, many prominent American companies do lots of business overseas).

So here is what I suggest for your Couch Potato Portfolio:

Name Percent of Portfolio

S&P 500 13%

U.S. Value 20%

U.S. Small Cap 12%

U.S. Small Value Cap 10%

U.S. Midcap 10%

Total International 25%

Emerging Markets 5%

REIT 5%

Just a little background info: The S&P 500 is made up of 500 of the largest American stocks. Pretty much any large company you can think of is a part of this index . Next, a value fund. A value fund is a group of stocks which are deemed undervalued (and have often fallen out of favor with the general public generally). Historically, these unpopular stocks have outperformed popular stocks by several percentage points annually. For the most part, publicly traded companies are small cap, mid cap, or large cap (or small companies, medium size companies, or large companies). Most of the companies we have all heard of are large cap companies. Emerging markets are nations with social or business activity in the process of rapid growth and industrialization. These are countries like China and India, which are growing at a much faster pace than the US. And last is a REIT, or Real Estate Investment Trust. This is a way of investing in real estate without actually owning the property directly.

It is important to note that this just includes the equity (stocks) portion of your portfolio. If you are just coming out of college, there is no reason to put too much money at all in bonds since historically, stocks outperform bonds by a large margin (see chart above). As you grow older, though, this should change to reduce risk.

This portfolio has everything a basic investor needs in an investment portfolio. And quite frankly, this is all any investor needs. Large (safer) companies, smaller (riskier) companies, value, international exposure, and a small dose of real estate. This is a portfolio that won't keep you up at night. It's called a couch potato portfolio because you don't have to worry about it. You could sit on your couch (or bed if you are moh) all year, not make any moves, and be perfectly content. The only thing you would need to do at the end of the year is "rebalance" your money so the percentages match the above percentages again. That's a discussion for another day though. The point is, if you buy into this philosophy, make regular contributions, AND LEAVE YOUR PORTFOLIO ALONE, this method will work, and there is a very high chance you will be financially better off than if you didn't use it.

So your next question may be, how do I go about implementing a plan like this? Well you will have to wait until my next blog to find out.

Take Care.

The key to this portfolio is diversification and the way you do that is by buying low-cost mutual funds/Exchange Traded Funds (ETFs) (these are made up of many stocks instead of individual stocks) across many different asset classes and from all over the world. You can't just buy the huge companies that we have all heard of, like Apple and Wal-Mart, because there isn't enough growth left in those businesses. Did you know that historically, those small companies that no one has every heard of have produced a better return than those big companies? Well it's true. Check out this chart that shows how much $1 invested across a given asset class in 1926 would have grown in the next 80 years. Small stocks clearly provide a greater return than large stocks historically. And you can't focus solely on American stocks because the United States' economy is already established and is growing at a much slower pace than over 100 countries around the world so it is wise to invest internationally (lucky for us, many prominent American companies do lots of business overseas).

So here is what I suggest for your Couch Potato Portfolio:

Name Percent of Portfolio

S&P 500 13%

U.S. Value 20%

U.S. Small Cap 12%

U.S. Small Value Cap 10%

U.S. Midcap 10%

Total International 25%

Emerging Markets 5%

REIT 5%

Just a little background info: The S&P 500 is made up of 500 of the largest American stocks. Pretty much any large company you can think of is a part of this index . Next, a value fund. A value fund is a group of stocks which are deemed undervalued (and have often fallen out of favor with the general public generally). Historically, these unpopular stocks have outperformed popular stocks by several percentage points annually. For the most part, publicly traded companies are small cap, mid cap, or large cap (or small companies, medium size companies, or large companies). Most of the companies we have all heard of are large cap companies. Emerging markets are nations with social or business activity in the process of rapid growth and industrialization. These are countries like China and India, which are growing at a much faster pace than the US. And last is a REIT, or Real Estate Investment Trust. This is a way of investing in real estate without actually owning the property directly.

It is important to note that this just includes the equity (stocks) portion of your portfolio. If you are just coming out of college, there is no reason to put too much money at all in bonds since historically, stocks outperform bonds by a large margin (see chart above). As you grow older, though, this should change to reduce risk.

This portfolio has everything a basic investor needs in an investment portfolio. And quite frankly, this is all any investor needs. Large (safer) companies, smaller (riskier) companies, value, international exposure, and a small dose of real estate. This is a portfolio that won't keep you up at night. It's called a couch potato portfolio because you don't have to worry about it. You could sit on your couch (or bed if you are moh) all year, not make any moves, and be perfectly content. The only thing you would need to do at the end of the year is "rebalance" your money so the percentages match the above percentages again. That's a discussion for another day though. The point is, if you buy into this philosophy, make regular contributions, AND LEAVE YOUR PORTFOLIO ALONE, this method will work, and there is a very high chance you will be financially better off than if you didn't use it.

So your next question may be, how do I go about implementing a plan like this? Well you will have to wait until my next blog to find out.

Take Care.

Monday, October 31, 2011

Jeff Foster, the Buffett of Basketball

Let me start out by saying that I never would have thought I would be writing a blog about Jeff Foster. Yes that Jeff Foster. The guy who has somehow managed to play 12 seasons in the NBA while averaging a whopping 4.9 points a game. But here I am writing about Jeff Foster. Why? Because it turns out he is a pretty smart guy.

The other day I came across this article: http://www.businessweek.com/magazine/jeff-foster-the-buffett-of-basketball-10202011.html. It's the story of how Jeff Foster, a below-average NBA player his entire career, wisely invested his money and lives within his means, and therefore, is not sweating out this lockout as much as most NBA players (Hey Moh, I hear the lockout is ending soon!). Foster has made about $47 million so far in his career, so you may be thinking, "he makes millions each year. Why does he have to worry about money?" Well because according to the NBA Players Association, about 60% of former NBA players go broke within five years of retirement. 60%! How amazing is that (although not as bad as the 78% of NFL players that supposedly go broke within two years of retirement). So Jeff Foster is a little different. He does not spend hundreds of thousands to millions on the latest "toys" that most millionaire athletes do. Instead, he invested millions in bonds, equity, real estate, and a few other things and is now financially protected for the future. And it turns out, believe it or not, that Foster can still afford to live in a fancy house, buy a few nice cars, and live a pretty awesome life despite saving millions of dollars. Crazy...

The problem with athletes these days is that a majority of them get their million dollar bonuses and contracts and then go on a continuous shopping spree until they inevitably go broke (Isn't that right Mr. Pippen? Why on earth did you think it was a good idea to buy a jet?!). What athletes really need is a boot camp on finances 101 right upon signing their first contract. Then each one needs to hire a money manager (not a scam artist!) of some sort who will make sure he will still have money when he is 40, 50, 60 and beyond. If only athletes knew how little of each paycheck they could stash away to make millions upon millions of more money...

That's why I find it kind of absurd that NBA players are struggling for cash during this lockout. Sure I get it that they aren't getting their millions these days but if you know there is a potential for a lockout every 5-10 years, don't you think it would have been wise to work that into your planning? Of course it would have. That doesn't mean the majority of them do it.

I give a little bit more respect to Jeff Foster after reading this article. I am sure there are others like Foster, but I know there are tons that aren't. Wouldn't it be wise for the NBA Players' Association to set up a mandatory Finances 101 boot camp for players entering the league? I think so. And maybe the league has something like this, but it's obviously not working.

Try to imagine another company. Say a manufacturing company that built widgets. This company had a few hundred employees and paid very well, which allowed most of its employees to retire at a very early age. However, within 5 years of retirement, 60% of retirees were broke. Don't you think the management of that company would take a step back and question what's going on? I think the NBA Players' Association needs to take a step back and start educating its players to be more like Jeff Foster.

The other day I came across this article: http://www.businessweek.com/magazine/jeff-foster-the-buffett-of-basketball-10202011.html. It's the story of how Jeff Foster, a below-average NBA player his entire career, wisely invested his money and lives within his means, and therefore, is not sweating out this lockout as much as most NBA players (Hey Moh, I hear the lockout is ending soon!). Foster has made about $47 million so far in his career, so you may be thinking, "he makes millions each year. Why does he have to worry about money?" Well because according to the NBA Players Association, about 60% of former NBA players go broke within five years of retirement. 60%! How amazing is that (although not as bad as the 78% of NFL players that supposedly go broke within two years of retirement). So Jeff Foster is a little different. He does not spend hundreds of thousands to millions on the latest "toys" that most millionaire athletes do. Instead, he invested millions in bonds, equity, real estate, and a few other things and is now financially protected for the future. And it turns out, believe it or not, that Foster can still afford to live in a fancy house, buy a few nice cars, and live a pretty awesome life despite saving millions of dollars. Crazy...

The problem with athletes these days is that a majority of them get their million dollar bonuses and contracts and then go on a continuous shopping spree until they inevitably go broke (Isn't that right Mr. Pippen? Why on earth did you think it was a good idea to buy a jet?!). What athletes really need is a boot camp on finances 101 right upon signing their first contract. Then each one needs to hire a money manager (not a scam artist!) of some sort who will make sure he will still have money when he is 40, 50, 60 and beyond. If only athletes knew how little of each paycheck they could stash away to make millions upon millions of more money...

That's why I find it kind of absurd that NBA players are struggling for cash during this lockout. Sure I get it that they aren't getting their millions these days but if you know there is a potential for a lockout every 5-10 years, don't you think it would have been wise to work that into your planning? Of course it would have. That doesn't mean the majority of them do it.

I give a little bit more respect to Jeff Foster after reading this article. I am sure there are others like Foster, but I know there are tons that aren't. Wouldn't it be wise for the NBA Players' Association to set up a mandatory Finances 101 boot camp for players entering the league? I think so. And maybe the league has something like this, but it's obviously not working.

Try to imagine another company. Say a manufacturing company that built widgets. This company had a few hundred employees and paid very well, which allowed most of its employees to retire at a very early age. However, within 5 years of retirement, 60% of retirees were broke. Don't you think the management of that company would take a step back and question what's going on? I think the NBA Players' Association needs to take a step back and start educating its players to be more like Jeff Foster.

Saturday, October 29, 2011

The Power of Compounding Interest

Want to know the secret to becoming rich? I'm talking about how your Average Joe can become rich. It's called compounding interest. Let me start with a simple example. Say at the beginning of year 1, you invest $100 (the principal) and you earn a return of 10% for that year. At the end of the year you will have $110 (100*1.1). $100 is your initial investment and you earned $10 interest. Simple right? Let's keep going. Say you don't invest any more money in year 2, and you just let your money grow at 10% again. At the end of year 2 you will have $121. $100 of that $121 is the initial money you put in. $20 of the $121 is the interest earned on your original $100 investment. So that leaves $1. That $1 is the power of compounding interest.

Compounding interest is when you earn interest not only on your principal (the $100) but also on the interest that you already earned. So after year 2 you are not only earning interest on your original $100 investment but also the $10 of interest that you earned after year 1. Now $1 may not seem like a lot, but things add up quickly.

Let me show you a real-life example. Say you graduate from college, and you start earning your first paycheck when you turn 22. At age 22, you start putting $300 a month into a Roth IRA (a type of retirement fund where you put money in after you paid taxes on that money). That brings your yearly contribution to $3,600. Lets further assume that you contribute $300 every month to your Roth IRA through your 30th birthday and then don't contribute any more money to your IRA for the rest of your life. If your investment earns an annual return of 10% (the average annual return of the stock market over time), how much would you have by the time you retired at age 65? Any guesses?

Maybe a few hundred thousand? You may think $200,000 would be a nice chunk of change that would be waiting for you at 65 after you only put in $32,400 total. Well I think you will be pleasantly surprised....... drum roll........$1.37 million! You could be a millionaire when you retire! Don't believe me? Here is the year by year breakdown of what you put in each year and your total at the end of the year:

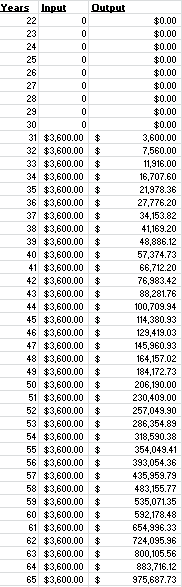

You can see that at the beginning, say the first 10 years after you stopped saving, your investment does not grow that large. This is because compounded interest needs time to work. The sooner you start saving the better! Let me show you another example that illustrates the importance of saving as early as possible. In this example, you start saving $300 a month when you turn 31 and continue to save $300 a month every month until you retire at age 65 (a total contribution of $126,000). If you earn 10% annually, how much money do you think you would have at 65? It has to be more than $1.37 million right? Maybe $4 million? $8 million. Let your imagination go......drum roll......$975,000. That's right. Less than a million dollars. Less than the first example! Here is proof:

The point is, start saving early because it does not make much initial money to make you a millionaire! Of course, compounding interest can also work against you if you have debt, so it's important that you pay off your debt as quick as you can. If you would like me to crunch some number for your unique situation, let me know!

Take care.

Maybe a few hundred thousand? You may think $200,000 would be a nice chunk of change that would be waiting for you at 65 after you only put in $32,400 total. Well I think you will be pleasantly surprised....... drum roll........$1.37 million! You could be a millionaire when you retire! Don't believe me? Here is the year by year breakdown of what you put in each year and your total at the end of the year:

You can see that at the beginning, say the first 10 years after you stopped saving, your investment does not grow that large. This is because compounded interest needs time to work. The sooner you start saving the better! Let me show you another example that illustrates the importance of saving as early as possible. In this example, you start saving $300 a month when you turn 31 and continue to save $300 a month every month until you retire at age 65 (a total contribution of $126,000). If you earn 10% annually, how much money do you think you would have at 65? It has to be more than $1.37 million right? Maybe $4 million? $8 million. Let your imagination go......drum roll......$975,000. That's right. Less than a million dollars. Less than the first example! Here is proof:

The point is, start saving early because it does not make much initial money to make you a millionaire! Of course, compounding interest can also work against you if you have debt, so it's important that you pay off your debt as quick as you can. If you would like me to crunch some number for your unique situation, let me know!

Take care.

Sunday, October 23, 2011

America: Home of the Financially Illiterate

It's kind of amazing to me how financially illiterate our country is. I'm not talking on a national level, although our government needs some help, but on an individual level. I am just now, in my senior year of college, taking my first wealth management class (I am not counting that joke of a class consumer ed that we had to take in high school). This got me thinking, why so late? We all need to learn this stuff sooner and be reminded of it more often. The average score on a financial literacy test for high school students was 48%. That is an F ladies and gentlemen. The average score on that same test for a college students? 62%. Better but still awful. My question is, why aren't kids being taught wealth management sooner? Money management is basic math. It's pretty simple, yet people don't know it.

Let me give you a test:

1. Suppose you had $100 in a savings account and the interest rate was two percent per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

a. More than $102

b. Exactly $102

c. Less than $102

d. I don't know

2. Imagine the interest rate on your savings account was one percent per year and inflation was two percent per year. After one year, would you be able to buy more than, exactly the same as, or less than today with money in this account?

a. More than today

b. Exactly the same as today

c. Less than today

d. I don't know

Got your answers? I'll give you another minute to really think those over. I will start by telling you that only 56% of Americans would get those two questions correct. Ready to see if you are in that 56%? The answer to question #1 is "a" and the answer to question #2 is "c." If you did not get both of those right, you are not alone. If you did, well then, it's only two basic questions so don't get cocky. One last question:

3. Do you think the following question is true or false: "Buying a single company stock usually provides a safer return than a stock mutual fund."

a. True

b. False

c. I don't know

This one should be a bit easier. The answer is "b." Now if you answered all three of those questions correctly, you are part of 34% of Americans who may be somewhat financially literate. That means 66% of Americans don't know this stuff. Stephen J. Dubner in Freakonomics makes a wise point. He says:

"I am all in favor of a well-rounded education, but seriously: what good is it if high-school students learn Flaubert, biology, and trigonometry if they don't learn how to take care of their money? One bright side to the increasingly dark economic news these days is that more and more people will learn (albeit the hard way) Rule #1: Do not buy what you cannot afford."

In middle school and high school we learn about biology, chemistry, physics, algebra, geometry, history, english, and maybe a foreign language, but where is the class that teaches financial literacy? Sure some schools have economics, maybe a basic accounting class, and a consumer education class, but I would bet that those classes aren't teaching students what they really need to know and what they will need to apply when they get older. Heck, I'm a finance major, and I'm learning about essential aspects of financial literacy as a senior in college! Two things are wrong with that. One, I am a senior in college. Why wasn't I taught this earlier? It's not like I haven't been earning and spending money for the past 6+ years. Aspects of financial literacy should be introduced in elementary school and be a mandatory subject to take every year until you graduate high school. Second, I am a finance major, and I am learning this stuff. Not that I don't need to know this stuff, because I definitely do, but what about all the other non-finance majors? Do they not get to learn the stuff I'm learning? It's kind of like "the rich get richer" because most finance students already know a decent amount about money and how it works, so they don't need to know these things as much as non-finance majors and yet, they are the students who get taught how to manage money. My point is, everyone needs to be financially literate, not just finance and accounting majors. Everyone. Everyone will most likely earn money some point in their life and everyone needs to know how to handle it! I'm dumbfounded that this stuff isn't taught to more students.

Dubner goes on to list 5 pieces of financial literacy that he believes should be taught in schools. They are:

1. Basics of how markets work. Things like: it is the law of demand and supply that determines prices in competitive markets, and the interest rate is the price of money.

2. Time value of money and the working of interest compounding: Because so many payments in finance happen at different points in time, one needs to know how to compare payments. Discounting is at the basis of asset pricing. What is the price of bonds? It is the present value of its payments. Interest compounding is a fundamental concept and it requires a little bit of math. It is critically important to understand interest compounding to be able to fully appreciate the importance of starting to save young and how to borrow and handle debt.

3. The concept of risk and the working of risk diversification and insurance: A lot of the decisions about saving and investing have to do with how to handle risk.

4. Basic accounting: To know the net values one needs to subtract assets and liabilities, and that it makes a big difference between whether we choose market prices versus book prices.

5. Rights and responsibilities of consumers and institutions. People need to know there is a Federal Deposit Insurance Corporation, bank deposits are safe (up to $100,000), and there is no need to line up to withdraw deposits; they should know who does and does not have fiduciary duties and what it means to use a financial advisor (you cannot sue them if the stock market plummets).

Now how many of you can tell me you know this stuff? Very few I imagine, and that's a problem.

So the point of this blog is to share information. Share information that most would consider an afterthought. But also I want to start a conversation. I want to know what you think. I will continue to post interesting and debatable topics in the coming weeks and months, and I would love to hear your thoughts and feedback! Leave a comment or feel free to send me an email at dan.boduch@gmail.com.

Take Care.

Subscribe to:

Comments (Atom)